Planning - Apr 24, 2026

What is the Money For?

By Tara Bansal

Published April 24, 2026

April is Financial Literacy Month.

Which means everywhere you look, there’s another article, checklist, or post telling you how to improve your financial literacy—save more, invest smarter, optimize everything.

But today, I want to do something different.

Because in my experience—both personally and professionally—more information is not our problem.

I’m a financial planner, and I still want objective, outside help.

I want someone I trust—someone who can help me see my blind spots and think more deeply about my life, not just my money.

Because the question I come back to, over and over again, is simple:

What is the money for?

I consider myself similar to many of the people we work with—highly educated, driven, and successful by most definitions.

I care deeply about my family and our future, and I also want to enjoy our life now.

Time feels more and more precious—with aging parents, quickly growing teenagers, and full schedules. I’m juggling more than I want, and finances are one part of life that touches every other part.

I want to feel confident that I’m doing the right things. I want to be responsible.

And if I’m honest, I also want some relief from the pressure—and reassurance that we’re on the right path.

That’s why Financial Literacy Month can sometimes feel like more pressure, not less.

I am feeling this in my own life right now.

There are times when things feel clear and steady—and then there are times when something shifts, and that sense of confidence gets shaken.

We are in one of those moments.

There is more uncertainty than there used to be. More questions. More second-guessing.

Are we spending too much?

Are we making the right decisions?

Will our plan still work the way we thought it would?

And underneath all of that is a deeper tension I know so many people feel:

I want to be responsible.

And I also don’t want to miss this precious time.

Our boys will only be home with us for a finite number of years. That feels very real to me right now. I want to be present. I want to create memories. I want to enjoy our life together while we’re in it—not just plan for the future.

And at the same time, I care deeply about our future—about security, freedom, and making thoughtful decisions that support the life we want long-term.

Holding both of those at the same time is not easy.

What has stood out to me the most is this:

Even with the knowledge, even with the planning, even with years of experience—there are still moments where it feels heavy and a little scary.

Not because I don’t understand the numbers.

But because it’s not just about the numbers.

It’s about uncertainty and the pressure to get it right.

It’s about the stories we tell ourselves in those moments—what I often call “head trash”—that can feel very real, even when they’re not fully true.

And what I’ve come to realize is this:

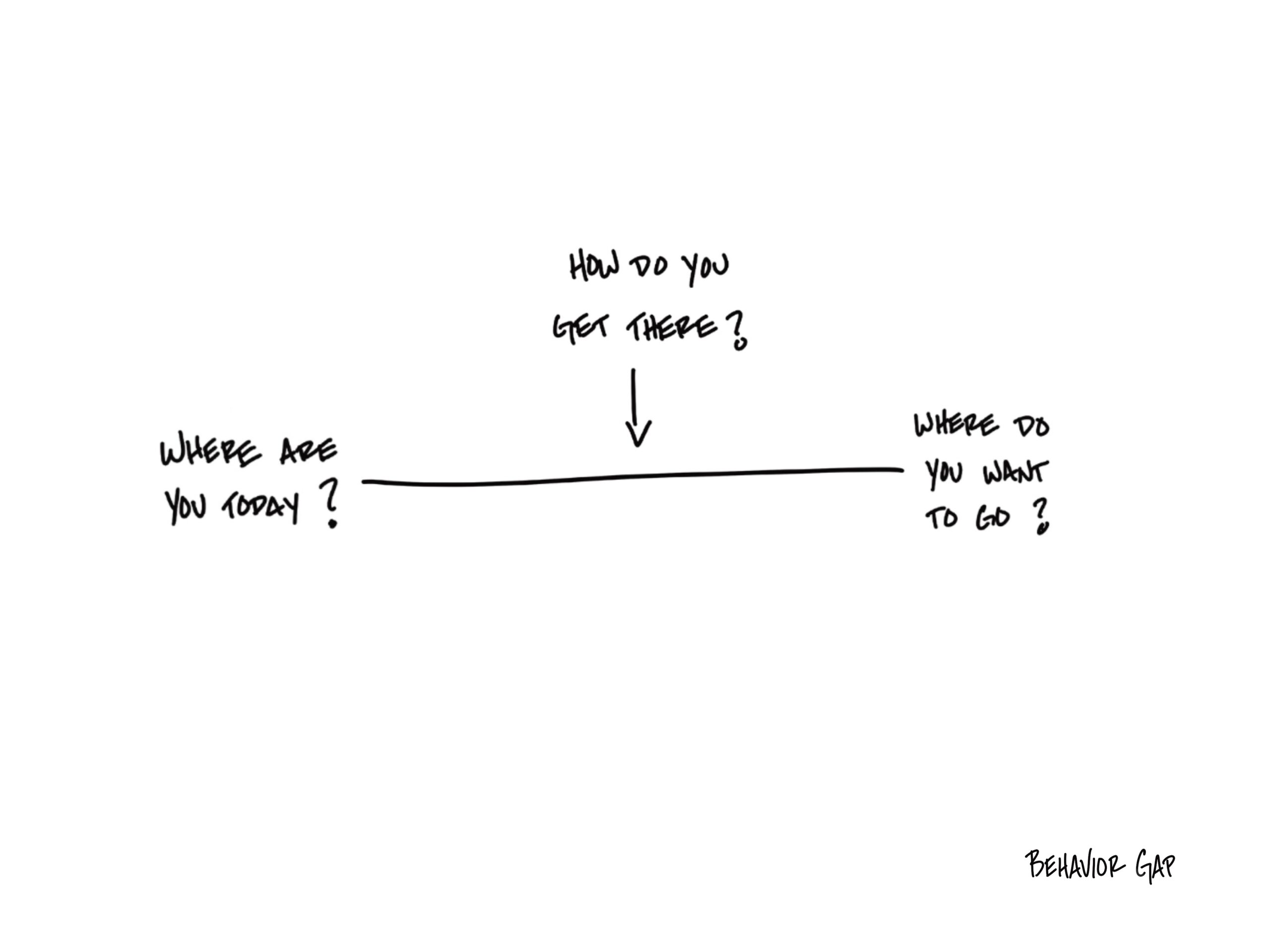

Clarity about what the money is for doesn’t remove uncertainty.

But it gives us something to come back to.

It helps us make decisions with intention instead of reacting out of fear.

We all have access to more information than ever before—AI, podcasts, articles, Google.

If information solved the problem, most of us would feel clear and confident by now.

But we don’t.

Because the real challenge isn’t knowledge. It’s the emotions around money. It’s seeking clarity and alignment. It’s knowing what actually matters – and intentionally making decisions from that place.

One of the most important things I do with my clients is helping them align their money with what matters most to them — because only they know what that is.

What feels meaningful, what feels worth it, what brings them joy or peace of mind — those answers are deeply personal. A valuable advisor’s role is to listen, understand, and build a plan around them.

And if they’re still figuring some of that out? That’s completely normal. We’ll discover it together.

That’s where we begin—with curiosity, with space to think, and with better questions.

Because the most important part of financial “literacy” isn’t what you know.

It’s whether your money is aligned with what matters most to you and your family.

So this month, instead of focusing on tactics—saving more, Roth conversions, insurance decisions—I want to offer you something simpler, and yet harder.

Take a few minutes to step back and reflect:

What is the money for?

How do you want to feel about your finances—and how do you actually feel right now?

Is there a gap between those two?

What do you want your children to understand about money—and are you living that in your own life?

And if not, what might be getting in the way?

If this resonates—if you’re feeling the pressure, the responsibility, or the quiet weight of trying to get everything “right”—you’re not alone.

And you don’t have to carry it alone.

If you’re craving more clarity, more honesty, and a plan that actually supports the life you want to live, that is the work we care most about.